Self-Directed IRAs and Solo 401(k)s give you the power to invest in alternative assets like real estate, cryptocurrencies, startup companies, and more. Generally, these accounts are opened to save for retirement on a tax-deferred (Traditional IRA) or tax-free (Roth IRA) basis.

However, there are certain circumstances where the investment income in your IRA may incur additional taxes, including UBIT (Unrelated Business Income Tax). Let’s take a look at what UBIT is and scenarios when it could apply to your investment.

According to the IRS, unrelated business income is “the income from a trade or business regularly conducted by an exempt organization and not substantially related to the performance by the organization of its exempt purpose or function”.

Unrelated Business Income Tax (UBIT) is often used interchangeably with the term Unrelated Business Taxable Income (UBTI). UBIT is the tax owed based on the unrelated business income received by the tax-exempt account. UBTI is the type of income that is taxable.

Congress created UBIT in the 1950s to prevent tax-exempt entities such as non-profit corporations, charities, universities, and retirement accounts from having an unfair advantage over taxable entities like corporations. Without UBIT, the for-profit companies would have to pay income tax on the same type of unrelated business activities that the non-profit organizations partake in but do not have to pay taxes on, which would give an advantage to non-profit organizations.

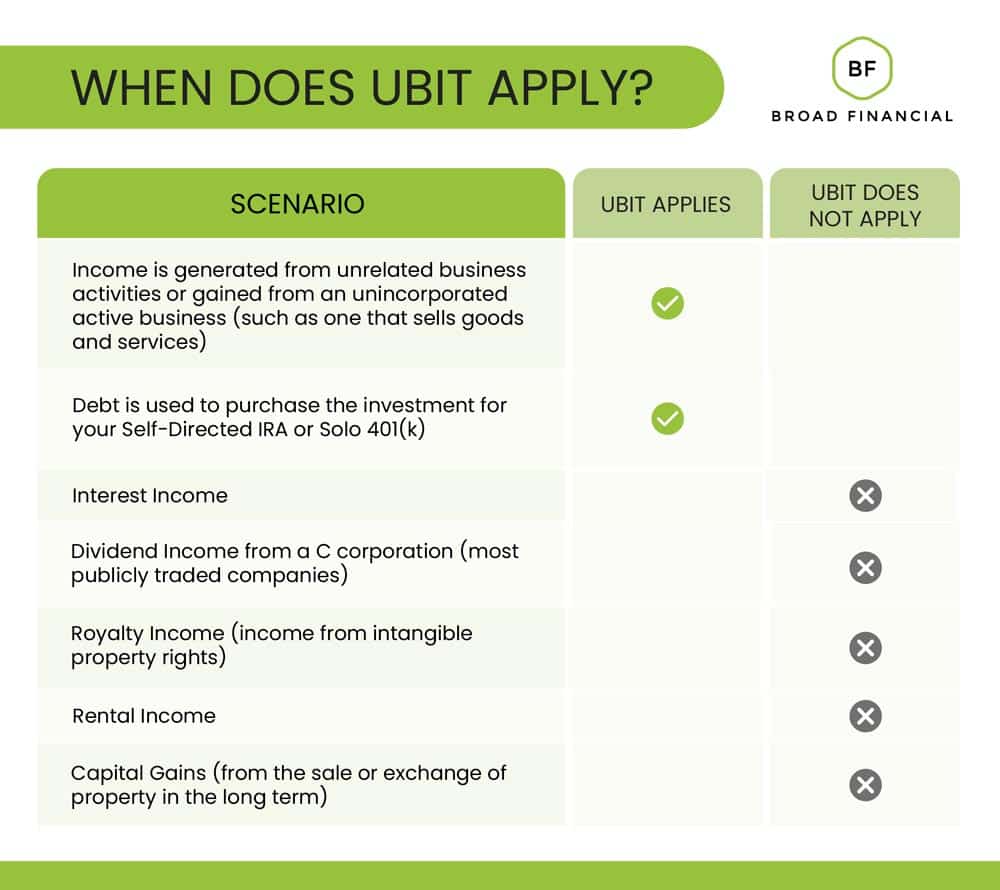

Self-Directed IRA account holders typically do not have to pay UBIT because most alternative investments are passive. However, there are a few scenarios where UBIT does apply. To find out if UBIT applies to your investment, consider asking yourself the following questions.

If the income is deemed as active or earned from performing a service or sale of products, UBIT applies.

For example, assume a tax-exempt organization or entity (such as a non-profit organization or a Self-Directed IRA/Solo401(k)) invests in an operating business (sells goods and services like a restaurant, tech company, gas station, etc.) that is structured as a pass-through entity for tax purposes (e.g., LLC or partnership) and does not pay corporate taxes. The income that flows from the LLC to the IRA is ordinary income, therefore UBIT is due.

Another example of an active alternative investment is real estate that is bought for a purpose other than to serve as a long-term investment. The property may be bought for construction, development, or with the intent to be acquired and then immediately sold (e.g., fix-and-flip). To determine if UBIT applies to your real estate investment, the IRS would likely look at the following factors:

The second scenario when UBIT occurs is when a tax-exempt entity uses debt to purchase an investment. For example, if a non-recourse loan was used to help your Self-Directed IRA purchase a real estate investment, then the portion of net profits attributed to the borrowed money, known as Unrelated Debt Financed Income, is subject to UBIT.

If your account is subject to UBIT, the tax rate varies depending on how much income you made from the business. The lowest tax rate is 10%, which applies to income of $2,900 or less, but the tax rate can run as high as 37%, which is the amount assessed on income beyond $14,450.

Once you calculate the amount of taxes owed, your IRA LLC must file IRS Form 990-T by April 15 (plus any IRS-granted extensions). The first $1,000 in annual gross UBIT income is exempt. Certain states may have their own type of UBIT. Contact a financial advisor to see if this applies to your state.

The IRA is the owner of the investments. Therefore, UBIT is owed by the IRA, not by the account holder. The tax is paid using IRA funds, not personal funds.

IRAs that are invested in a business (e.g., an LLC or partnership) that produces ordinary income should be provided with a K-1. The LLC or partnership preparing the K-1 should use the identification number of the IRA custodian (not the social security number of the IRA account owner) to report the IRA’s taxable income.

UBIT should not deter you from investing your Self-Directed IRA in alternative assets that generate ordinary income, as many investors can miss out on profitable opportunities to diversify and grow their retirement portfolios. As stated before, most alternative assets are passive and do not incur UBIT. However, if UBIT is due there are two possible ways you can avoid it. Please consult a financial professional to understand your options, the rules, and the taxes incurred by your investment.

Do you have more questions about UBIT? The self-directed Specialists at Broad Financial can help. Schedule a free call with us today!

Address:

One Paragon Drive

Suite 270

Montvale, NJ 07645

Phone: (800) 395-5200

Mondays – Thursdays: 8:00 am – 6:00 pm EST

Fridays – 10:00 am – 4:00 pm EST